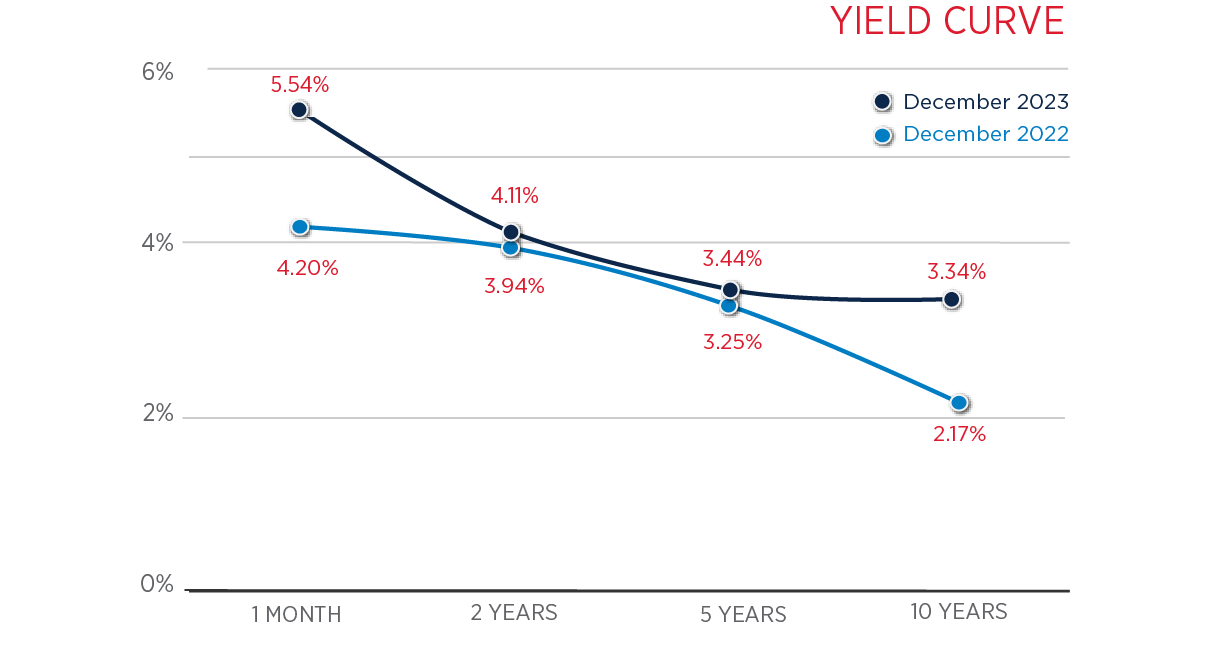

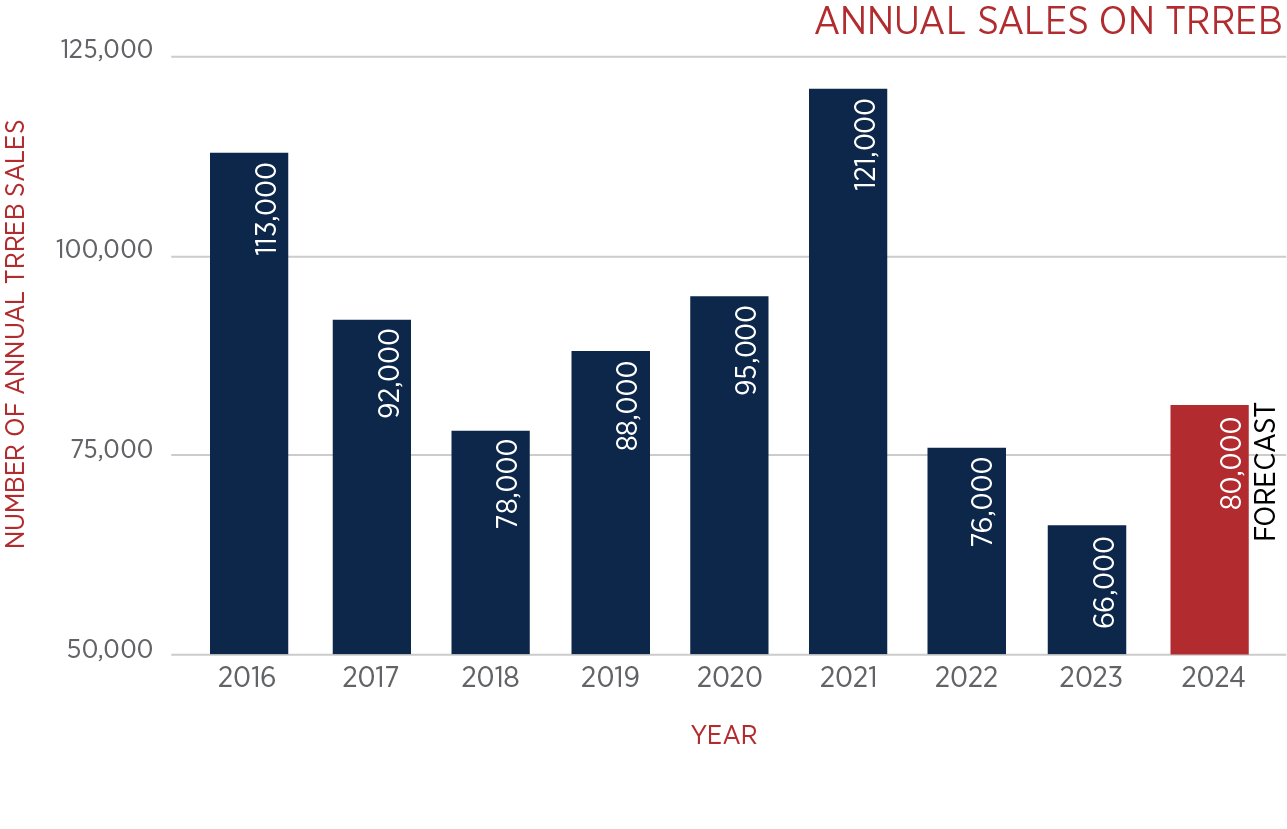

It’s beginning to look a lot like…the start of interest rate cuts.After the US Federal Reserve (the “Fed“) took its foot off the “interest-hiking” pedal on Wednesday December 13, 2023, following a similar decision by the Bank of Canada (“BOC“), inflation seems like it is well in hand. Now, the Fed seems to be suggesting that they may lower interest rates in the U.S. three times in 2024. Is the same going to happen in Canada in 2024? That remains to be seen. The Governor of the BOC stated on Friday December 14, 2023, that it is “too early to consider cutting our policy rate.” But, is not following or preempting a rate cut by the US something that the BOC can in fact avoid? Time will tell. However, it seems that the time of rate increases has passed. Rate cuts are likely to come in 2024. So, what is now a “buyer’s market” may quickly morph into a “sellers market”. As financing is key for buyers, obviously, if rates are set to drop (at some point), perhaps buyers are well served by locking in deals now with longer closing periods to allow them to capture the potential for lower rates later in 2024. Or alternatively, buyers may want to look for shorter term financing arrangements to lock in lower home/asset values now, so that they can take advantage of lower rates down the road – when asset prices will no doubt climb. We have said this before, and many have echoed this, the housing market in Canada, and particularly in the GTA is likely to turn around quickly and with ferocity. There is a pent up demand and a lack of supply. When financing begins to flow more freely and cheaply, that demand is going to eat up whatever supply there is, causing prices to increase. It seems that buying in this market allows buyers/investors to be more selective and diligent in considering the location of the asset, the price, and type. It also provides more negotiating power, whereas once the market returns to a seller’s market, that power will evaporate. With a price difference on average around 25% between the re-sale market and the pre-construction market right now, perhaps it is a good time to look into the offerings on the re-sale market for some great deals. As always, the Dash team is here to help you along your real estate investment journey. Please reach out to us with any questions or thoughts. In the meantime, we wish you a Happy Holiday Season! |

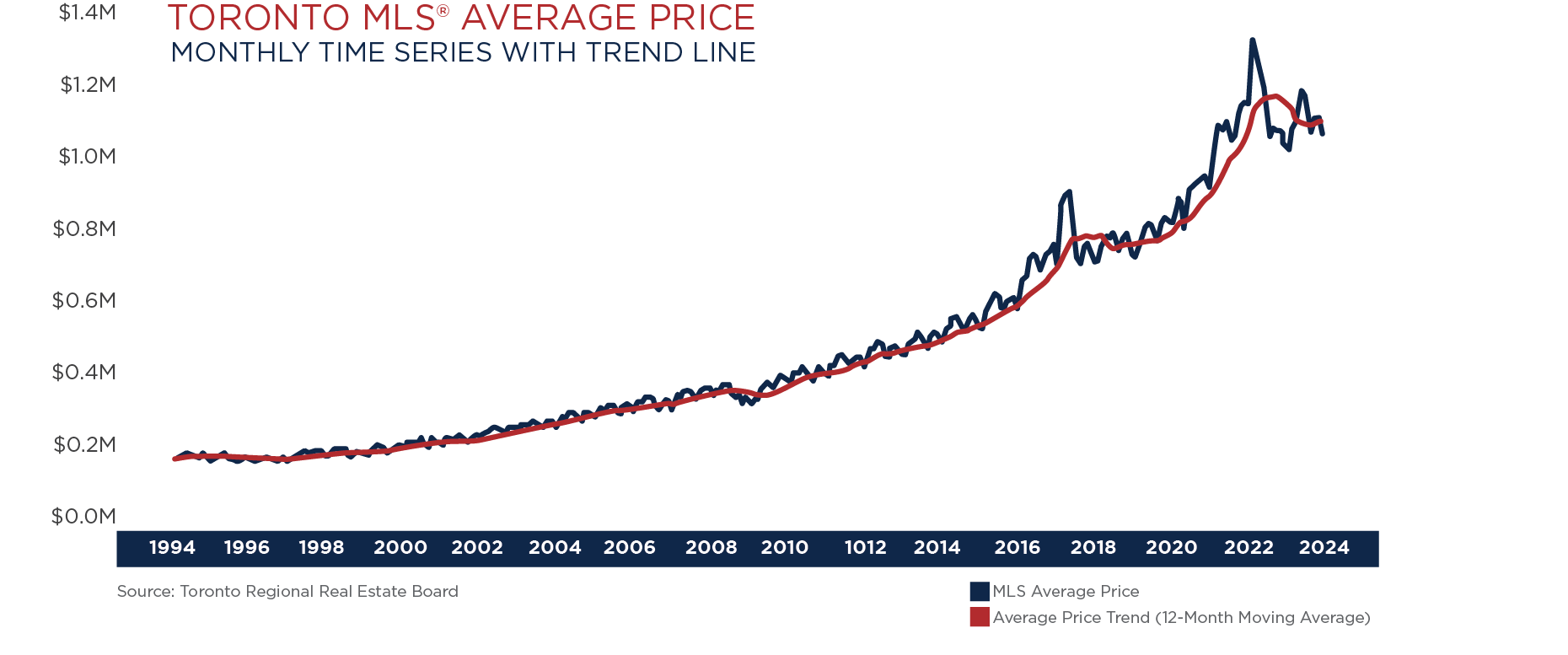

Source: Toronto Regional Real Estate Board

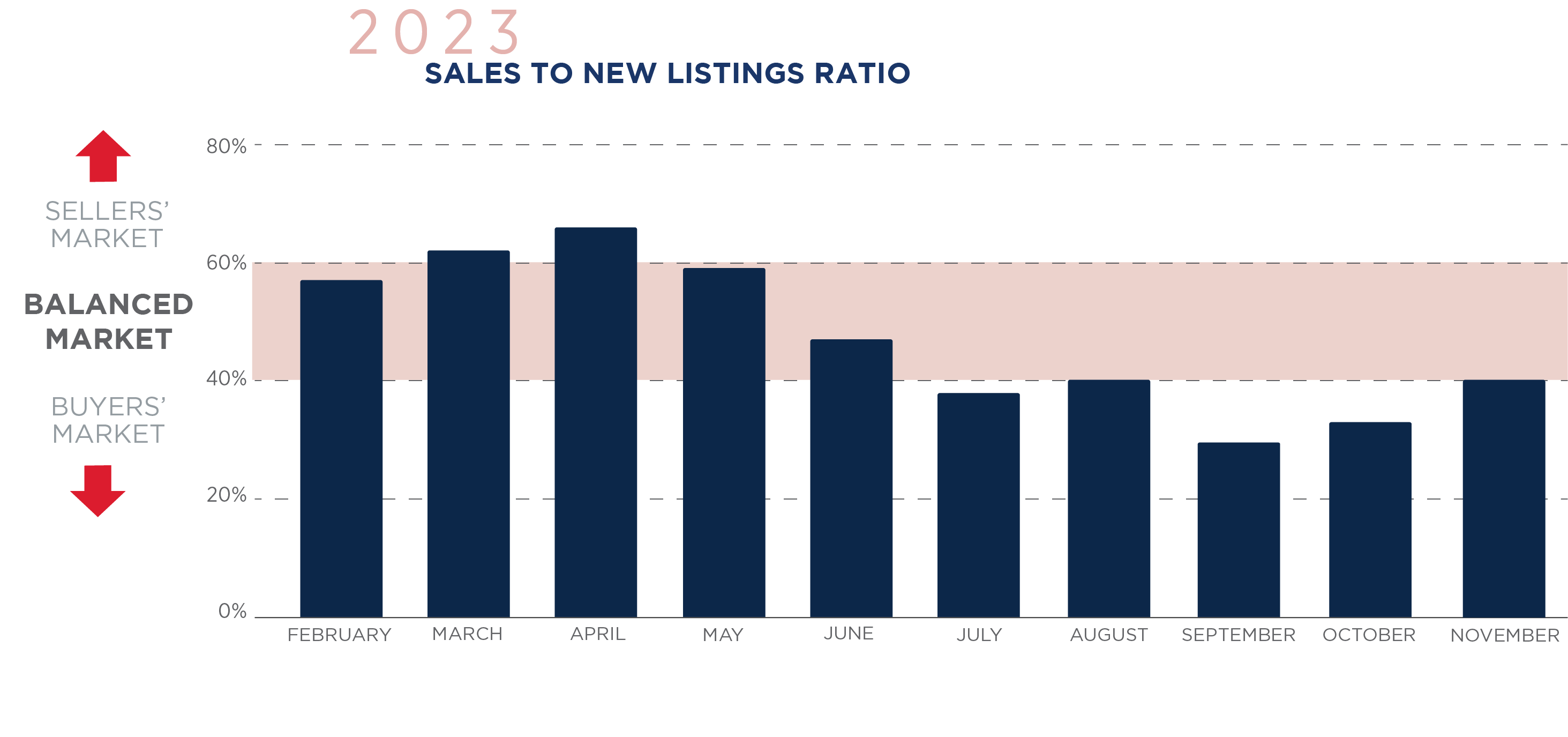

Source: Toronto Regional Real Estate Board