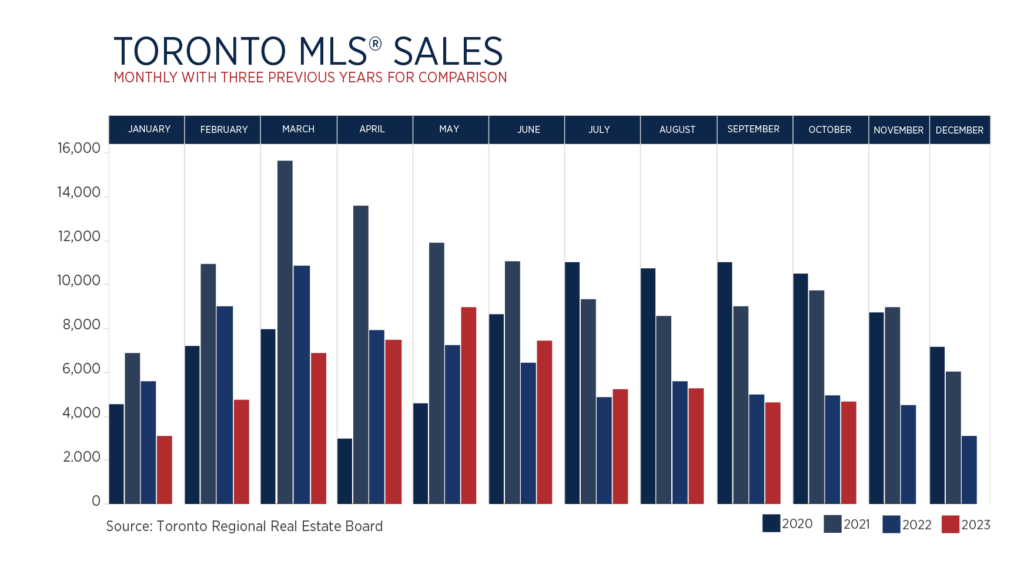

The Real Estate HibernationWith inflation seemingly on the decline both here in Canada and south of the border and interest rates seemingly having peaked, it looks like the real estate market has gone into hibernation in advance of winter 2023. Based on assessments of listings and sales in the months of September and October, we are seeing both buyers and sellers largely stepping back and waiting out the winter in the hopes for a spring acceleration. However, it seems the conditions in the market have swung largely in favour of buyers. Mortgage renewals into 2024 and beyond will see existing owners re-financing at higher rates than when they purchased in 2019 and 2020. This will inevitably induce the sale of properties by poorly capitalized owners, favouring well capitalized buyers who are able to withstand higher short term mortgage rates. Housing demand remains very high in Canada, especially in the GTA. Which, in due course, will only serve to drive prices higher until supply catches up, notwithstanding some near term softness. We at Dash don’t have a crystal ball to predict or prognosticate on what the interest rate or housing market will hold in the future. Most economists seem to believe that interest rates will moderate down towards the end of 2024; especially given the flood of refinancing expected in the next two years. If interest rates come down, more buyers will enter the market to compete for a limited supply of properties. Timing the market is nearly impossible. And, the Dash team is here to help you assess whether now is a good time for you to buy or sell your property based on your unique needs and goals. Please reach out to us to discuss your plans, and let us help you maximize your returns. More than ever before we are being invited by leading developers to assist them with positioning rental guarantee programs for their projects. We would be excited to share these opportunities with you. Our team is welcoming all Nobu Condos purchasers to assist them with leasing out their suites and realize the appreciation to their investment. Until then, we hope you have an incredible November! |