Market Overview

On Wednesday April 12, 2023, the Bank of Canada declared that it was keeping interest rates unchanged. This is the second meeting where the BOC confirmed they will hold the line. In tandem, growth projections for Canada were upgraded, increasing the chances of a soft landing, rather than a broad and hard hitting recession. The BOC has heard the market, especially in light of the recent global bank turmoil, and is prepared to wait and see how inflation tempers at current rates. The key seems to be: can the economy continue to grow faster than expected without pushing inflation up. With increased immigration, the answer may be, “Yes”.

While maintaining interest rates at their current rates will certainly put some financial pressure on landlords with variable rate mortgages. We do not see this as being a significant broader market risk and we anticipate market improvements in later 2023 for these reasons:

- Canadian Banks have been flexible with their borrowers in an effort to avoid broad defaults on mortgages. Banks traditionally do not want to own or operate real estate.

- In practical terms, if landlords are forced to sell property, that forces tenants to vacate properties, which in turn reduces the supply of rental units on the market, increasing demand. In response, rental rates in the City of Toronto will escalate. Alternatively, those same renters may become buyers of real estate if rental rates are sufficiently high, which would further put upwards pricing pressure on real estate in the GTA.

- Canada set a new immigration record in 2022 with more than 430,000 permanent residents arriving. This is only a portion of the number of immigrants that entered Canada in 2022. Canada is the fastest-growing G7 country and saw population growth over 1.05 million people in 2022, almost entirely due to immigration and temporary residents.

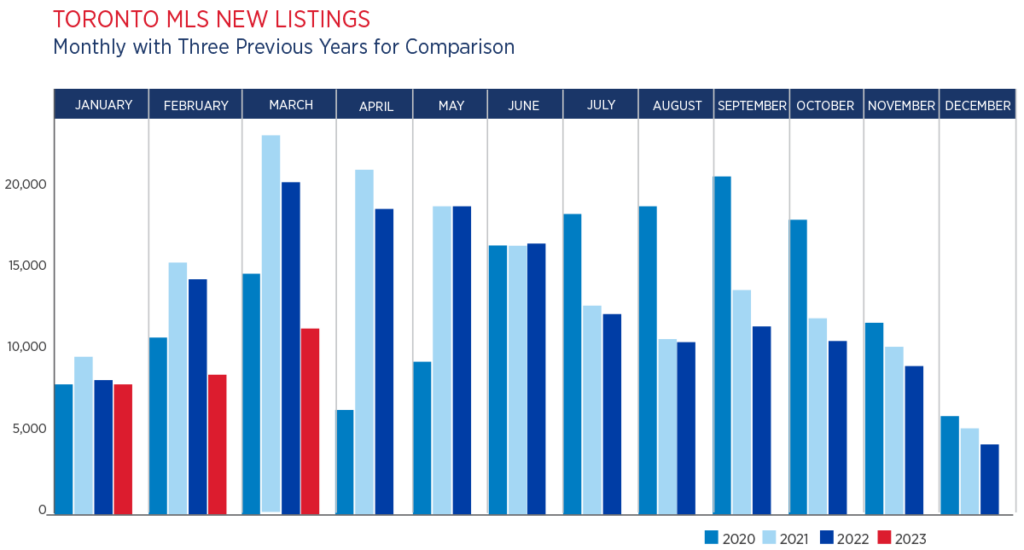

- The number of properties listed for sale in March of this year was at the lowest it has been in approximately 20 years. The longer there is a reduced supply in the market, the more pressure there will be for real estate prices to rise, despite the higher interest rate environment in which we find ourselves.

Certainly, the world could change and there could be a significant amount of supply that reaches the real estate market at one time. However, given the population growth and the already problematic imbalance of supply to demand in housing, it seems unlikely that the GTA’s real estate market will suffer in the long term and if early indicators are correct, we may see price escalation towards the end of 2023 with interest rates moderating in 2024.

|

|